Context of use of Cube Platform

An Investment Bank who provides broker services primarly to institutional clients on ETD instruments needs to manage all the second-level Risk Management processes

Company functions involved

Listed Derivatives (ETD) Desk, Risk Manager, Credit Office

Front Office functionalities

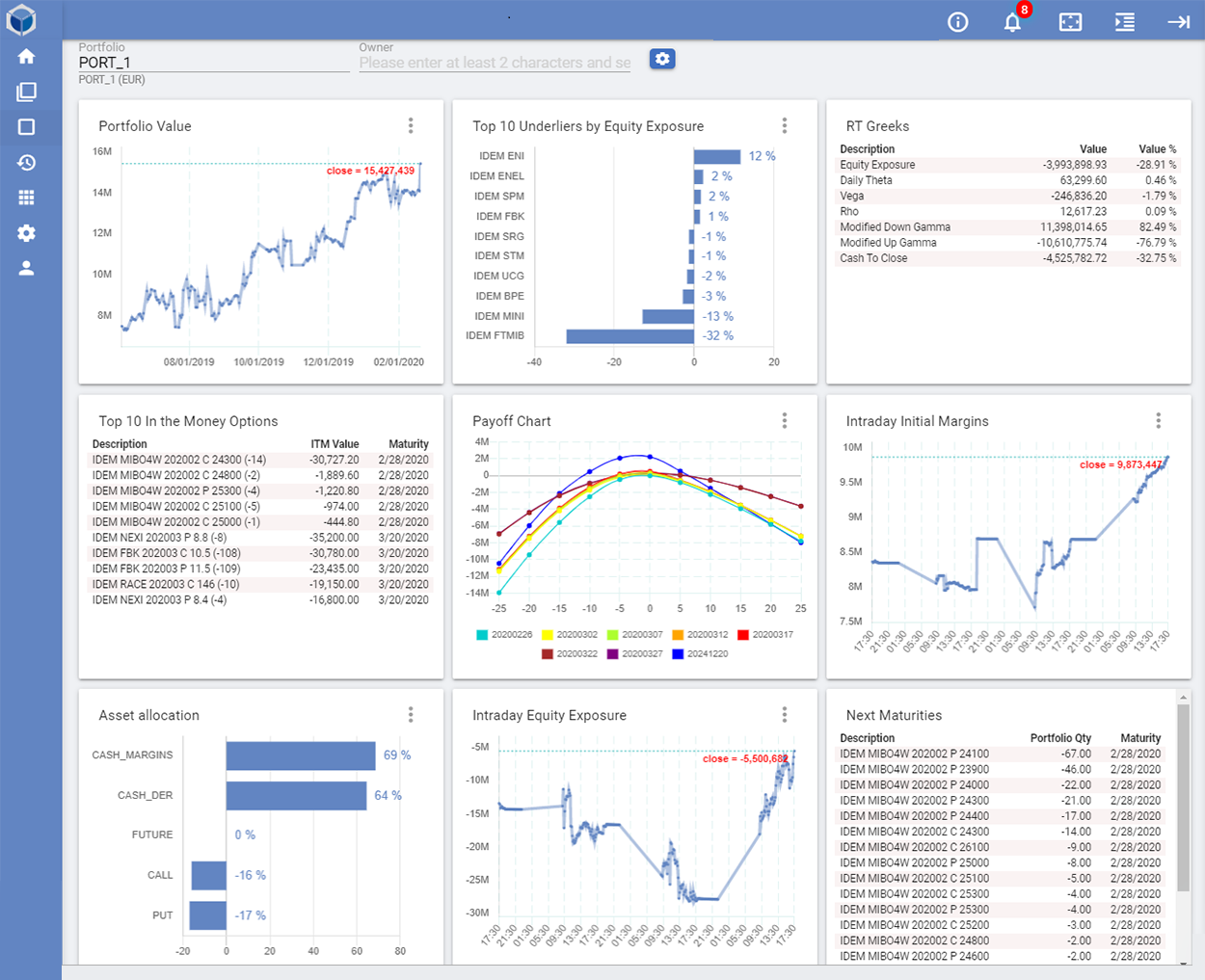

- RT monitoring of all portfolios in Margin Call

- Pre-trade margin verification

- RT portfolio monitoring of all risk metrics (qty, PL, exposure)

- Simulate effect of virtual positions on current portfolios

- Help customers reduce any kind of risk (Delta, Gamma, Vega, Value at Risk)

- Help customers reduce required margins

- Manage the entire order life-cicle, from its generation to the fill

- Send/receive orders to/from any brokers automatically via FIX (EMSX, TSOX, FIX hubs)

Risk Management functionalities

- RT monitoring of post-trade operational limits set by the bank

- RT monitoring of post-trade Value at Risk

- Portfolio Value at Risk calculation with various models (Parametric, Historical Simulations and their sub-versions)

- Test the VaR model used through Back Test process and validation

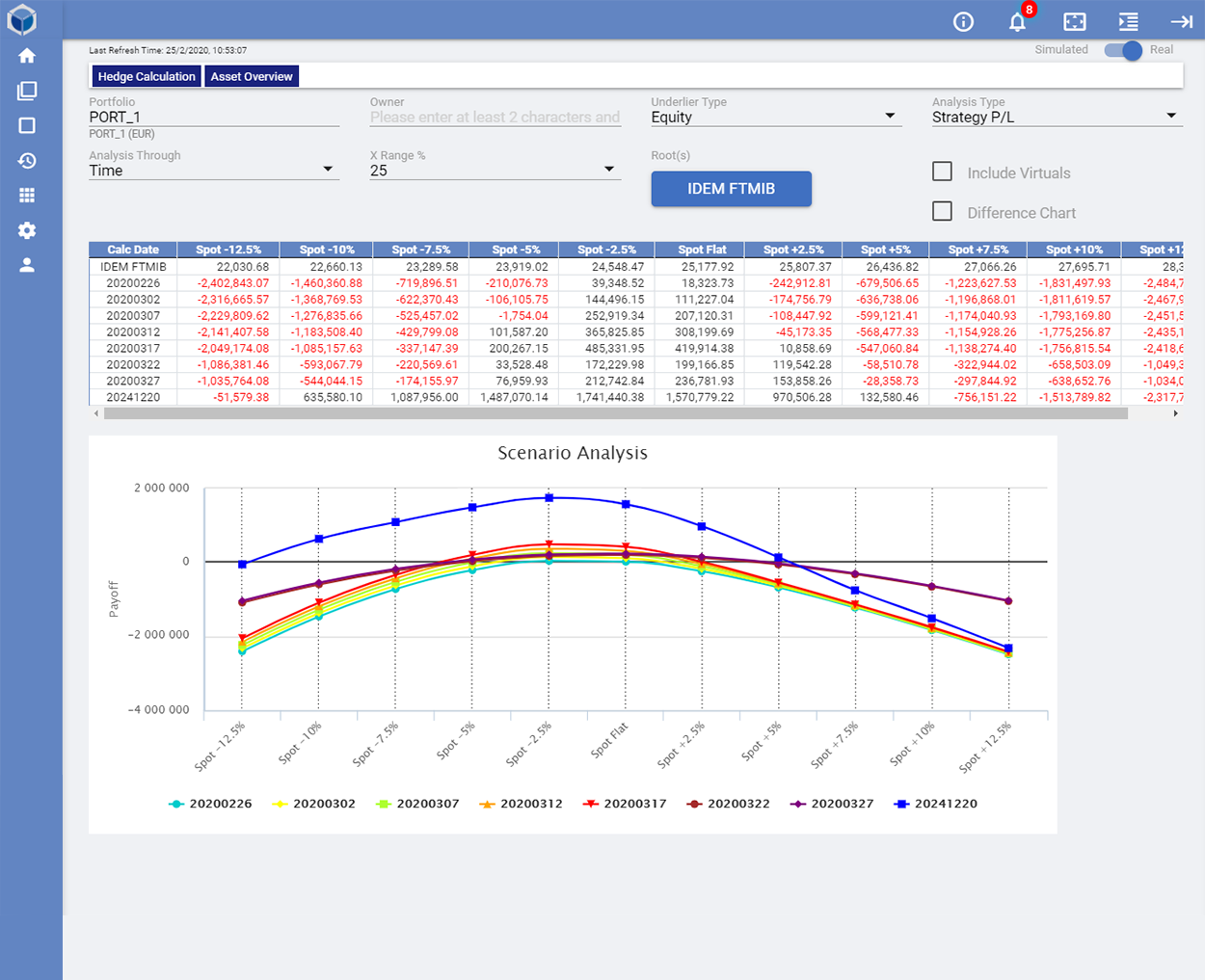

- Scenario Analysis

- Stress Test Analysis